The Hidden Dilution Trap: Stacking Post-Money SAFEs at Different Valuation Caps

Nearly half of founders raising on SAFEs use multiple valuation caps — often without realizing that post-money SAFEs protect investors from dilution at the founders' expense. Here's how the math works, why it matters, and what you can do about it.

The post-money SAFE — introduced by Y Combinator in 2018 — has become the default instrument for early-stage fundraising. Its appeal is simplicity: if an investor puts $500K into a $5M post-money cap, they own exactly 10%. Clean, predictable, easy to explain on a napkin.

But that simplicity hides a structural problem that most founders don't discover until it's too late: when you stack multiple post-money SAFEs at different valuation caps, every dollar of dilution comes exclusively from the founders.

The Data: Most Founders Are Stacking SAFEs

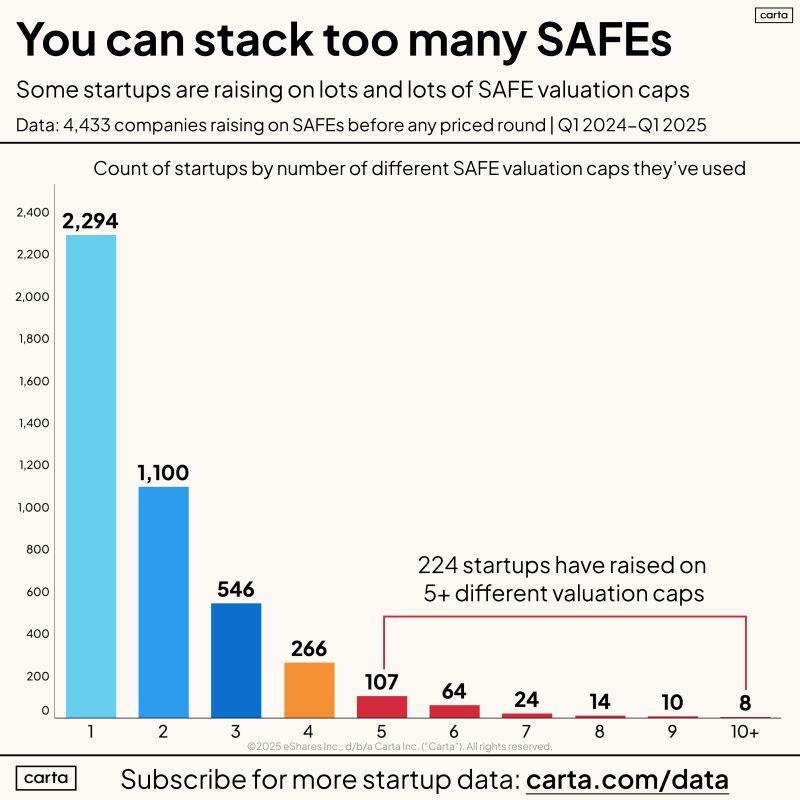

Recent Carta data paints a striking picture. Of 4,433 companies that raised on SAFEs before any priced round (Q1 2024–Q1 2025):

- 2,294 raised at a single valuation cap

- 1,100 raised at two different caps

- 546 raised at three different caps

- 224 raised at five or more different caps

That means roughly half of all founders raising on SAFEs are doing so at multiple valuation caps. Many of them are unknowingly creating massive founder dilution.

The Lemonade Stand Problem

The best way to understand why post-money SAFEs create outsized founder dilution is with a simple example, adapted from EC/VC Law.

Suppose you open a lemonade stand. Your parents give you $50 for 50% of the venture. You use the $50 to build the business. Then a customer is so impressed with your lemonade that they offer you $100 for a 10% stake — implying your company is now worth $1,000.

Most people would agree the resulting split should be: 45% parents, 45% you, 10% customer. The parents' investment helped build a $1,000 company, and they should be diluted proportionally by the new investment, just like you are. That's how equity rounds work.

But if your parents invested $50 on a post-money SAFE with a $100 cap, and the customer invested $100 on a post-money SAFE with a $1,000 cap, the result is: 50% parents, 10% customer, 40% you. Your parents aren't diluted at all. You absorb the entire impact of the new investment.

That 5 percentage point difference may seem small in a lemonade stand. In a venture-backed startup raising millions across multiple rounds, the gap becomes enormous.

Worse Than Full Ratchet Anti-Dilution

As José Ancer at Silicon Hills Lawyer has argued, the anti-dilution protection embedded in post-money SAFEs is more extreme than anything considered "standard" in startup finance:

Under YC's new SAFE, the common stock absorbs all dilution from any subsequent SAFE or convertible note rounds until an equity round, while SAFE holders are fully protected from that dilution. It's the equivalent of "full ratchet" anti-dilution, which has become almost non-existent in startup finance because of how company unfriendly it is. In fact, it's worse than full ratchet because in a typical anti-dilution context it only triggers if the valuation is lower. In this case, SAFE holders get fully protected for convertible dilution even if the valuation cap is higher.

This is a critical point that founders miss. In a traditional anti-dilution provision, protection only kicks in during a down round — when the company raises at a lower valuation. With stacked post-money SAFEs, earlier investors are protected from dilution even in up rounds. That's unprecedented in startup finance, and it's baked into the standard template.

The Core Mistake: Treating SAFEs Like Equity Rounds

The fundamental error founders make is assuming that raising on a new SAFE at a higher valuation cap works like raising an equity round at a higher valuation. It doesn't.

In a priced equity round, when new investors come in, everyone gets diluted proportionally — founders, employees, and earlier investors alike. If a Series A investor owns 20% and the company raises a Series B, that 20% gets diluted along with everyone else. Later money dilutes earlier money. This makes economic sense — the earlier investors' capital helped build value, and they share in the dilution when new capital enters.

With stacked post-money SAFEs, this doesn't happen. Each SAFE investor's percentage is carved out of the founders' ownership, not out of the total pie. Earlier SAFE investors sit comfortably at their locked-in percentage while the founders absorb the full impact of every subsequent SAFE.

As Jay Yeh has noted, the shift from pre-money to post-money SAFEs was marketed as a way to give founders "easier math" — and it did. The dilution calculation is dead simple: investment ÷ cap = ownership percentage. But founders are paying for that simpler math with percentage points of their company.

A Concrete Example

Let's say you have 10 million founder shares and a 10% option pool (1 million shares, 11 million total). You raise $500K, then $1M, then $1.5M — at valuations of $5M, $10M, and $15M respectively. Let's compare what happens if you do all three as post-money SAFEs versus doing one initial SAFE and then switching to priced equity rounds.

Scenario A: Three Post-Money SAFEs

| Round | Amount | Post-Money Cap | Investor Ownership |

|---|---|---|---|

| SAFE 1 | $500K | $5M | 10.0% |

| SAFE 2 | $1M | $10M | 10.0% |

| SAFE 3 | $1.5M | $15M | 10.0% |

Each investor's percentage is locked in. SAFE 1 stays at 10% when SAFE 2 is issued. SAFE 1 and SAFE 2 both stay at 10% when SAFE 3 is issued. All the dilution stacks on the founders:

- SAFE 1 investor: 10.0%

- SAFE 2 investor: 10.0%

- SAFE 3 investor: 10.0%

- Option pool: 6.4%

- Founders: 63.6%

Scenario B: One SAFE, Then Two Equity Rounds

Same amounts, same valuations — but after the initial SAFE, the founder pushes for priced equity rounds instead of more SAFEs.

| Round | Type | Amount | Valuation |

|---|---|---|---|

| Pre-Seed | Post-Money SAFE | $500K | $5M cap |

| Seed | Equity | $1M | $10M pre-money |

| Series A | Equity | $1.5M | $15M pre-money |

The SAFE converts at the seed equity round. The SAFE investor's 10% gets diluted by the seed round, and then both the SAFE investor and the seed investor get diluted by the Series A. Later money dilutes earlier money — just as it should.

- SAFE investor: 8.3% (diluted from 10.0% by two subsequent rounds)

- Seed investor: 8.3% (diluted from 9.1% by Series A)

- Series A investor: 9.1%

- Option pool: 6.7%

- Founders: 67.6%

The Difference

| Three SAFEs | SAFE + Equity | Difference | |

|---|---|---|---|

| Founders | 63.6% | 67.6% | -4.0 pts |

| SAFE investor | 10.0% | 8.3% | +1.7 pts |

| Second investor | 10.0% | 8.3% | +1.7 pts |

| Third investor | 10.0% | 9.1% | +0.9 pts |

The founders lose 4 percentage points of ownership — transferred directly to investors — simply because they used SAFEs for every round instead of switching to equity. And this is a modest example with only three rounds. The more SAFEs you stack at different caps, the wider this gap grows.

The key insight: in the equity scenario, the pre-seed SAFE investor's ownership drops from 10% to 8.3% as new money comes in. That's normal and economically fair — their early capital helped build value, and later investments dilute them proportionally, just like the founders. With all post-money SAFEs, that same investor stays at exactly 10% and the founders absorb everything.

Why Founders Miss This

-

Each SAFE looks small in isolation. Ten percent here, ten percent there — it doesn't feel alarming until you add it all up.

-

Rising valuations create a false sense of progress. "We raised at $5M, then $10M, then $15M" sounds like the company is growing. And it may be. But the cap structure means founders are paying a hidden premium for that narrative.

-

SAFEs are easier and cheaper than equity rounds. This is their whole appeal — and it's a real benefit. But founders conflate "easier process" with "same economic outcome." The process may be simpler, but the economics are fundamentally different, and not in the founders' favor.

-

Most founders don't model the full cap table. They know their current SAFE terms but haven't projected what the ownership breakdown looks like when everything converts at the Series A. By then, it's too late — the SAFEs are signed.

Solutions: What Founders Can Do

1. Push for a Priced Round Instead

If you're raising a meaningful amount of capital — especially if you've already raised on SAFEs — consider pushing for a priced equity round. Yes, it's more expensive legally and takes longer to close. But in a priced round, earlier investors are diluted by later investors, which is the economically fair outcome. The legal costs are a rounding error compared to the equity you might save. Seed equity templates exist that are dramatically simpler than full Series A docs.

2. Use Pre-Money SAFEs

The pre-money SAFE (YC's original version before 2018) doesn't lock in investor ownership percentages. Multiple pre-money SAFE holders dilute each other, which distributes the dilution impact more fairly — like an equity round. The tradeoff is less certainty for investors about their exact ownership, which is why many investors prefer the post-money version. But as a founder, that uncertainty works in your favor.

3. Redline the Post-Money SAFE

You don't have to throw out the post-money SAFE entirely. Silicon Hills Lawyer has published a simple redline — just a few words changed — that eliminates the anti-dilution problem while preserving the "clarity of ownership at closing" benefit that post-money SAFEs were designed to provide. The fix makes post-closing issuances proportionately dilutive to both founders and investors, just as they would be in any other financing structure. This corrected post-money SAFE is arguably the best of all worlds: simple closing process, clear ownership on Day 1, and fair dilution going forward.

4. At Minimum: Model Everything

Before signing any SAFE, model your full cap table including all existing SAFEs, the option pool, and the proposed new SAFE. Use a SAFE dilution calculator to see exactly where you'll land. If the numbers surprise you, that's your signal to negotiate harder or explore alternatives.

The Bottom Line

The post-money SAFE is a great instrument for a single raise at a single valuation cap. It gets dangerous when founders stack multiple SAFEs at escalating caps without understanding that they alone bear the dilution.

Nearly half of SAFE-raising founders are doing exactly this. The standard post-money SAFE template gives investors a level of anti-dilution protection that is more aggressive than anything considered normal in startup finance — and most founders don't know it until their Series A converts and the cap table comes into focus.

Model your financings. Understand the mechanics. And if the math doesn't work, push for a structure where it does — whether that's a priced round, a pre-money SAFE, or a corrected post-money SAFE that eliminates the hidden anti-dilution.

Need help modeling your SAFE stack or negotiating your next round? Book a free call — we help venture-backed founders navigate exactly these situations.

Need legal guidance for your startup?

Book a free intro call and see how Flux can help.

Book a Free Call